- TIPS & TRICKS/

- Essential AI Banking Solutions for the Modern CIO/

Essential AI Banking Solutions for the Modern CIO

- TIPS & TRICKS/

- Essential AI Banking Solutions for the Modern CIO/

Essential AI Banking Solutions for the Modern CIO

AI in banking has quietly crossed the line from innovation lab to everyday infrastructure. Virtual assistants handle high volumes of routine enquiries, treasury platforms forecast cash across multiple banks, and fraud systems score transactions in real time. These are not speculative pilots: they are live products with hard numbers behind them, from hours removed from manual workflows to measurable improvements in customer satisfaction and risk outcomes.

For the modern CIO, the challenge is no longer “whether” to use AI, but how to orchestrate it across front, middle, and back office without ripping out cores, multiplying vendors, or fragmenting data. AI capabilities now arrive embedded in digital banking suites, treasury portals, case‑management tools, and workflow platforms. The opportunity is to turn this patchwork into a coherent, governed product portfolio.

This article focuses on essential, proven AI solutions available today, seen through the lens of a 2–3 year roadmap:

- Concrete use cases across customer service, personalisation, risk, AML, treasury, underwriting, and operations.

- Example tools and patterns for embedding AI into existing channels and platforms.

- Practical approaches to model choice, data unification, and governance.

The core argument: AI should be woven into your current digital channels and platforms, powered by unified, well‑governed data, and sequenced by business value and organisational readiness - not pursued as standalone experiments on the side.

The CIO’s New AI Reality: From Experiments to Productised Solutions

AI in banking has moved from curiosity to core capability. The most advanced institutions are no longer asking whether AI works, but where to embed it next in the value chain. Industry analyses now show that a majority of large banks have formal AI roadmaps in place, with adoption concentrated in risk, customer engagement, and operations rather than isolated innovation pilots.

AI in banking today: where it is already working

Banks now run AI at scale across front, middle, and back office.

In parallel, banks are learning how to blend different model types and adaptation techniques - frontier LLMs, domain‑specific models,

and retrieval‑augmented generation - so they can productionise AI without rebuilding their entire stack.

Net effect: AI is already a proven lever for cost, risk, and revenue, not an R&D line item.

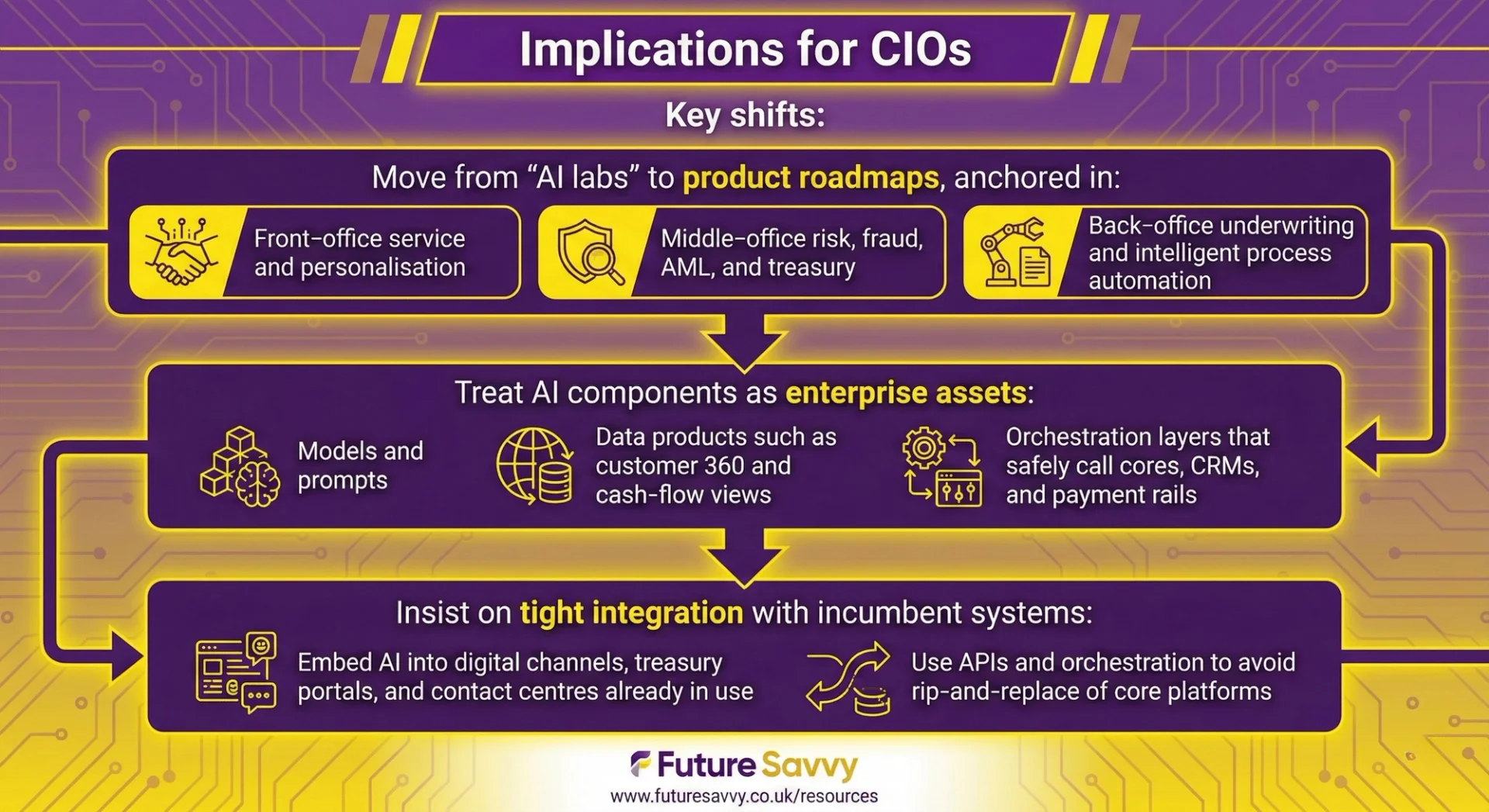

Implications for CIOs

This maturity changes the CIO agenda. The task is no longer to sponsor isolated pilots, but to select and scale solution categories that align directly to priority journeys - onboarding, servicing, lending, and treasury - while fitting within today’s architecture.

Key shifts:

The rest of this article will use a value‑chain lens - front office, middle office, back office, plus cross‑cutting platform and governance choices - to map which AI solutions belong where, how they integrate, and how CIOs can sequence them on the roadmap.

Front‑Office AI: Service, Engagement, and Personalisation

Front‑office AI is now a product decision, not an experiment. CIOs can plug mature capabilities directly into mobile apps, web banking, and contact centres, with measurable gains in service quality, sales, and efficiency. In market studies, fewer than a third of banks report tangible AI impact, but those that do are already using front‑office AI to industrialise customer service and revenue generation, rather than running isolated pilots, reinforcing that this layer is now a competitive battleground rather than a sandbox.

Conversational service: from basic chatbots to intelligent assistants

Modern banking assistants sit inside existing digital channels and contact centre platforms, handling routine queries while keeping humans in the loop for complex cases. Leading digital platforms are already embedding this pattern: FIS Digital One, for example, now ships with native AI agents via its integration with Glia’s AI for All platform, using virtual assistants to absorb repetitive enquiries while routing complex issues to human agents with full context preserved.

Core solution types:

- Tier‑1 chatbots embedded in mobile and online banking for 24/7 self‑service.

- Voice and chat assistants in contact centres, with seamless, context‑rich hand‑off to agents.

Typical capabilities include balance and transaction queries, card controls, simple servicing (PIN resets, travel notices), and guided navigation to the right feature or form. When they escalate, they carry the customer’s history into the agent desktop to avoid repetition and shorten handling times.

Business Insider’s overview of AI in banking highlights these assistants as one of the most widely deployed front‑office use cases, with large banks using them to reduce cost‑to‑serve while lifting customer satisfaction scores.

Product patterns to consider:

- Digital banking platforms with native AI chat, such as FIS Digital One integrated with Glia, offering in‑app messaging and co‑browse.

- Embedded assistants in the user interface, like Apiture’s “Ask AI”, supporting both customers and staff with contextual guidance.

Integration notes for CIOs:

- Primary insertion points: mobile and web banking SDKs, IVR and contact centre systems.

- Required data and systems:

- Customer profile and CRM data.

- Product catalogue and entitlement rules.

- Core account APIs for balances, transactions, and simple servicing.

- Key KPIs: containment rate, average handle time, CSAT, and strict adherence to advice boundaries and regulatory disclosures. The CFA Institute’s practical guide for LLMs in finance emphasises this blend of guardrails and retrieval‑augmented generation as a default pattern for compliant, customer‑facing assistants, particularly where they touch on products, pricing, or regulated advice

Personalised insights and offers

AI‑driven personalisation moves beyond static PFM widgets to continuous, in‑channel coaching and offers that reflect real behaviour and eligibility. In practice, banks are using machine‑learning models on transaction and relationship data to trigger prompts, nudges, and offers that materially change customer behaviour rather than just decorate the UI.

Core solution types:

- Personal financial management tools that surface AI‑driven insights.

- Next‑best‑offer and next‑best‑action engines embedded into digital journeys.

Common capabilities:

- Transaction categorisation, cash‑flow projections, spend alerts, and savings nudges based on observed patterns.

- Tailored product recommendations, such as credit line adjustments, savings and investments, or insurance, triggered by life events or risk indicators.

Banks can use:

- Digital platforms with built‑in marketing intelligence, like Apiture’s AI‑driven offers engine.

- Aggregated customer views, such as ASA One View’s 360° snapshot, to drive relevant journeys

- Specialist providers similar to Personetics that plug into data lakes and digital channels.

These patterns echo what AK Patel describes as the shift from “surface automations to end‑to‑end development and processing”, where AI changes not only the marketing copy but the design of offers, eligibility rules, and fulfilment flows in one joined‑up system.

Integration considerations:

Data foundations

- A governed customer 360 and clean transaction history.

- Connectivity to campaign tools or a customer data platform.

Governance:

- Clear responsible marketing policies and consent management.

- Explainable logic for why a given offer was shown, to satisfy both customers and regulators.

Agentic customer experiences: assistants that can act, not just answer

The next step is assistants that complete tasks end‑to‑end, within strict policy and control frameworks, rather than merely answering questions. Early deployments in both retail and corporate banking show that this “agentic” pattern is already live in the market, not hypothetical.

Core concept:

- Translate natural language (“Move £200 to my savings every payday”, “Dispute this card charge”) into validated, auditable operations over existing banking APIs. Prometeo’s Agentic Banking fabric and Payman AI’s orchestration layer are both designed around this principle, turning prompts into policy‑checked payments, transfers, and treasury moves across multiple institutions.

Example capabilities:

- Initiating payments and transfers, validating new payees, and enforcing daily limits.

- Amending standing orders and mandates, triggering dispute or chargeback workflows, and confirming outcomes to the customer.

Orchestration layers to evaluate:

- Tools like Payman AI that map user intent to specific, policy‑checked operations on your existing core and payments rails.

- Multi‑bank orchestration similar to Prometeo, enabling cross‑bank payments and validations with strong audit, role‑based controls, and ISO‑aligned security.

Integration priorities for CIOs:

- Robust authorisation, strong customer authentication, and explicit consent flows, with clear guardrails and transaction limits.

- Comprehensive, immutable audit trails and real‑time explainability for operations teams and regulators.

- Phased rollout:

- Start with low‑risk, reversible tasks (eg internal transfers, card reissues).

- Progress to higher‑value, higher‑risk actions only once governance, monitoring, and incident playbooks are proven.

In practice, an effective front‑office roadmap combines these layers:

- Conversational service to absorb routine demand.

- Personalisation to deepen engagement and product penetration.

- Agentic capabilities to turn conversations into secure, completed actions.

Middle‑Office AI: Fraud, AML/KYC, and Treasury Intelligence

AI in the middle office is now firmly product‑led rather than experimental. For CIOs, the opportunity is to harden risk and compliance while giving treasury teams sharper, faster intelligence - all without replacing existing case management or treasury platforms. Industry research suggests that more than half of financial institutions already use AI in risk and compliance, with front‑ and middle‑office use cases delivering the most tangible value so far, particularly in fraud, AML, and treasury tools.

Fraud detection and AML/KYC augmentation

Modern fraud and AML stacks combine classic machine learning for real‑time decisions with LLMs for richer investigations. This aligns with what regulators and industry bodies are starting to expect: explainable models wrapped with strong data governance and monitoring, rather than ungoverned “black boxes.

Core solution types & Key capabilities to target:

- Real‑time anomaly detection on cards, payments, and login behaviour

- Network and entity‑resolution tools to uncover hidden relationships

- LLM‑based assistants for case triage and analyst support

- Dynamic risk scoring on individual transactions and sessions, updating as new behaviour appears

- Graph‑based views of counterparties, beneficial owners, and suspicious networks across products and geographies

- Retrieval‑augmented search over policies, historic suspicious activity reports, and regulatory guidance to speed decisions

In practice, this often means plugging an entity‑resolution and network analytics layer into your existing AML and fraud engines, then adding an LLM front‑end that summarises cases, explains risk drivers, and recommends next steps using internal knowledge bases. As one industry leader puts it, “the deeper opportunity comes from deeper implementation, moving from surface automations to end‑to‑end development and processing”, with AI re‑engineering risk products rather than just patching workflows.

Integration priorities for CIOs:

- Standard connectors into transaction processing, screening engines, and case management tools

- Read/write access to data lakes or warehouses for model training, monitoring, and back‑testing -increasingly including high‑quality synthetic datasets to test rare scenarios safely within regulatory expectations

Clear KPIs:

- Fraud loss reduction

- False positive/negative rates

- Case handling time and backlog

- Quality and timeliness of regulator feedback

Treasury and liquidity management

AI‑driven treasury tools are one of the clearest middle‑office ROI stories, especially where they are embedded into existing portals. Leading transaction banks are already reporting material time savings and adoption when forecasting is delivered as a native feature of their treasury platforms, rather than as a separate tool.

Core solution types & Typical capabilities:

- Cash‑flow forecasting for corporates and, increasingly, SMEs and affluent retail

- Multi‑bank liquidity management with scenario analysis

- Automated ingestion and normalisation of account data from multiple banks and ERPs

- Forecasting models that project inflows and outflows by client, currency, and entity

- “What if” simulations for rate changes, payment delays, or drawdowns

Leading banks now embed these capabilities directly into their treasury platforms, giving clients a single workspace to see balances, run forecasts, and plan actions. Similar AI forecasting is appearing in retail and SME propositions for budgeting and cash‑flow planning, often combined with open‑finance data to provide a holistic, multi‑institution view of cash and commitments.

Integration notes:

- Primary insertion points: treasury portals, ERP connectors, and open banking/Open Finance APIs

- CIO focus areas:

- Robust data connectivity and reconciliation

- Model governance and stress‑testing, including clarity on when classical time‑series models remain superior and when to layer LLMs as an explanation and workflow surface rather than for pure prediction

- UX that allows relationship managers to interpret and explain model outputs

- KPIs:

- Forecast accuracy across horizons

- Hours saved for clients and internal teams

- Improved utilisation and pooling of liquidity

Knowledge and policy intelligence

Compliance, risk, and operations teams are increasingly using LLM‑based assistants as internal “copilots” rather than customer‑facing tools. This pattern -private models, retrieval‑augmented generation, and tight governance -is fast becoming the reference architecture for regulated workloads in financial services.

Core solution typ & Key capabilities to target:

- LLM‑based assistants that sit over policy libraries, manuals, and document repositories

- Summarising new regulations and surfacing gaps versus current policies and controls

- Answering first‑line queries on AML/KYC standards, product rules, and documentation requirements

- Automating document triage -routing KYC packs, clustering alerts, or flagging incomplete submissions

Integration considerations:

- Deploy as internal web tools or chat widgets integrated with intranets, policy repositories, and document management systems

- Use retrieval‑augmented generation to ground responses in bank‑approved “source of truth” content

- Governance essentials:

- Clear ownership by risk/compliance

- Version control and curation of knowledge sources

- Monitoring for hallucinations, with guardrails and escalation paths to human experts

Download our Pragmatic LLM Strategy for Banks

Download now

Download nowBack‑Office AI: Underwriting and Intelligent Process Automation

Underwriting and credit decisioning

AI is turning underwriting from a batch, paper‑heavy process into a near real‑time, data‑driven service.

Modern solutions combine traditional scores with cash‑flow and alternative data, improving risk discrimination without abandoning existing models. This direction mirrors what leading banks report in their AI programmes, where credit underwriting and risk scoring sit alongside fraud and AML as core value pools for machine learning in the back office.

Machine‑learning engines can ingest current account flows, merchant takings, payroll and even external open‑finance feeds, then estimate probability of default and loss‑given‑default with higher lift than static scorecards.

At the same time, large language models are absorbing much of the manual document work. They can read bank statements, tax returns, company accounts and collateral reports, extract key features into structured fields, and generate concise underwriter summaries.

Practical guides for LLMs in financial services now treat this kind of document intelligence and summarisation as a primary adoption pattern, alongside retrieval‑augmented assistants for credit and risk teams. Underwriters then focus on edge cases and judgement calls rather than data collection.

For CIOs, the integration pattern is clear:

- Plug ML models into the loan origination system, loan management system and decision engine rather than creating parallel tools.

- Use the existing model risk framework to govern data lineage, monitoring, challenger models and performance back‑testing.

- Build feedback loops from repayment behaviour, restructurings and recoveries into the modelling pipeline to keep estimates current.

- Enforce explainable outputs, robust documentation and bias monitoring so enhanced decisioning stands up to regulatory and internal audit review. Supervisors are increasingly explicit that AI and ML models must meet the same standards of explainability and control as traditional scorecards, including where synthetic data is used in development.

The goal is not a black‑box replacement of current policies, but an AI‑assisted underwriting stack that is faster, more consistent and easier to evidence.

Intelligent process automation (IPA) across operations

In operations, the shift is from scattered RPA scripts to orchestrated, AI‑driven journeys.

Document‑intelligence services can now read inbound forms, letters and emails, classify intent, extract key fields and kick off the right workflow. Identity and verification steps are increasingly automated through image, document and data checks, reducing rework and abandonment in onboarding and servicing.

This reflects a broader move away from narrow task automation towards end‑to‑end journey re‑engineering: as one banking technology CEO puts it, “the deeper opportunity comes from deeper implementation, moving from surface automations to end‑to‑end development and processing”.

LLM‑based “front doors” sit on top of legacy workflow and RPA, turning free‑text requests into structured tasks and routing them across existing BPM tools, case managers and bots. This pattern maps closely to how major banking platforms are embedding AI into digital channels today: AI agents classify and resolve routine requests, escalate complex ones with context, and orchestrate work across human and virtual teams. It works especially well for:

- Onboarding and KYC refresh

- Servicing changes (address, mandates, limits)

- Card disputes, reconciliations and simple claims

For CIOs, two architecture moves matter:

- Standardise on an orchestration layer that coordinates BPM, RPA, document AI and LLM interfaces, rather than adding more point automations.

- Prioritise high‑volume, rules‑heavy processes where data is already digital, and track KPIs such as cycle‑time reduction, error rates, manual touches and staff satisfaction.

This moves the bank towards end‑to‑end digital journeys without forcing a core replacement.

Segmentation by institution size

The same building blocks apply, but emphasis differs by size:

Turning the AI Map into Action

AI in banking has moved beyond experiments. It is now a core product and operations capability across the value chain, from customer conversations to treasury, risk, and back‑office processing.

The banks pulling ahead are not those with the most proofs‑of‑concept, but those with embedded, orchestrated, and well‑governed AI running in production – a pattern already visible in leaders using AI to industrialise fraud controls, credit decisioning, and customer engagement across their franchises

Underpinning this are strong data products, a pragmatic multi‑model strategy, disciplined governance, and integration into existing portals, cores, and workflows rather than wholesale replacement.

As one banking technology CEO puts it, “The deeper opportunity comes from deeper implementation, moving from surface automations to end‑to‑end development and processing,” where AI quietly orchestrates complex journeys while banks retain full control over risk and compliance.

AI banking solutions will keep evolving, but a disciplined, product‑led roadmap today will determine which institutions secure durable advantage over the coming years.

Get in touch today to learn more about how to make the most out of AI in banking and finance!

Frequently Asked Questions (FAQ)

Prompting, verification, workflow design, automation, and responsible AI use.

No. These skills apply across functions, from admin and marketing to finance and operations.

Clear examples of how you used AI to save time, improve quality, or support better decisions.

Begin with your current tasks, test AI on repeat work, and track the results.

Related Articles

Tips & Tricks

Tips & TricksAI Invoice Processing: The End of Manual Entry

Manual invoice processing is slow, error-prone, and limits visibility into cash going out the door. AI invoice processing automates data capture, PO matching, approval routing, and fraud/duplicate checks so AP teams can focus on exceptions instead of typing and chasing. The article explains how the technology works day-to-day, what features and KPIs matter most, and a practical roadmap to pilot, roll out, and prove ROI quickly.

Tips & Tricks

Tips & TricksTop AI Asset Management Platforms Reviewed

AI asset management patforms are moving into mainstream use as firms face fee pressure, tighter regulation, and the need to scale investment workflows with clear audit trails. The article compares platforms as products - focusing on real-world portfolio construction and rebalancing, transparent risk analytics, scalable personalisation and suitability, integrations, deployment options, economics, and governance.

Tips & Tricks

Tips & TricksData Analytics and AI: From Reporting to Predicting

Finance teams are stuck in static, backward-looking month-end packs that arrive too late to support fast decisions. By layering AI-enabled analytics on top of existing ERP/EPM, BI, and Excel - grounded in governed, “investment-grade” data - teams can automate reporting narratives, move to rolling forecasts, and add prescriptive recommendations directly in the flow of work. The winning approach is incremental: start with low-risk automation, build trust through explainability and audit trails, keep humans accountable, and scale what works via repeatable workflows.